Introduction

Source: https://mbaroi.in/blog/digital-payments-in-india/

Hi friends, hope all are fine and in good health.

“Digital India” was one of the hot topics which was launched by our Prime Minister in 2015.

One of the main concepts of ‘Digital India’ is to make the payment process simple and each transaction accountable by introducing cashless payments or digital payment systems.

It is aimed at digitizing the financial sector and economy with consequent benefits of efficiency, transparency, and quality.

In today’s blog let’s see about the evolution of digital payment in India.

Digital Economy

Source: https://www.shutterstock.com/image-vector/horizontal-2-colored-digital-economy-concept-1164878260

The digital economy is the worldwide network of economic activities, commercial transactions and professional interactions that are enabled by information and communications technologies (ICT).

The term was first coined in a book “The Digital Economy: Promise and Peril in the Age of Networked Intelligence” by author Don Tapscott in 1995.

There are three main components of this economy, namely,

- e-business

- e-business infrastructure

- e-commerce

It can be summed up as the economy based on digital technologies.

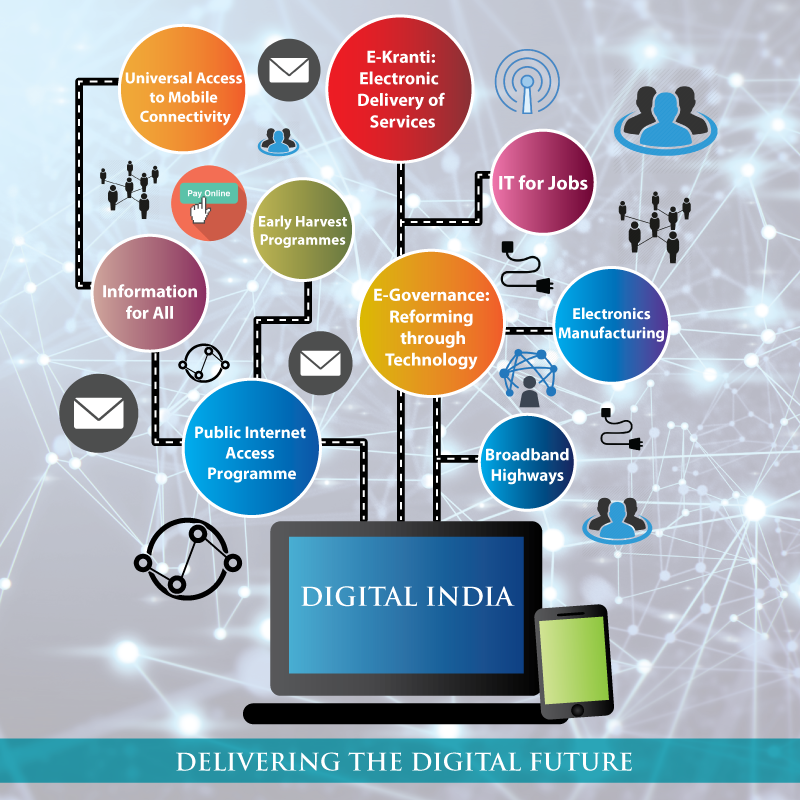

Digital India

Source: https://www.coai.com/node/563

Digital India is a flagship programme of the Government of India with a vision to transform India into a digitally empowered society and knowledge economy.

Launched on 1 July 2015, by Indian Prime Minister Narendra Modi, it is both enabler and beneficiary of other key Government of India schemes, such as BharatNet, Make in India, Startup India and Standup India, industrial corridors, Bharatmala, Sagarmala.

Vision of Digital India

The vision of Digital India programme is to transform India into a digitally empowered society and knowledge economy.

Vision Areas of Digital India

It consists of three core components: the development of secure and stable digital infrastructure, delivering government services digitally, and universal digital literacy.

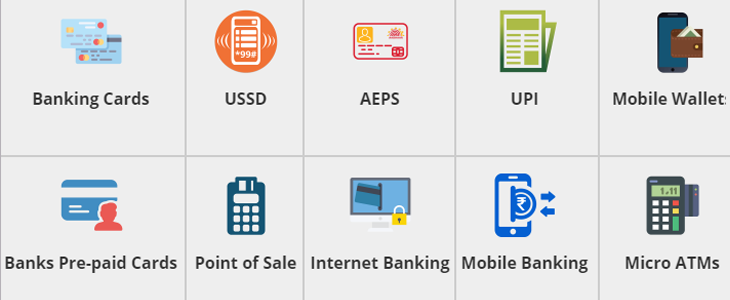

Digital Payments

Digital payments are transactions that take place via digital or online modes, with no physical exchange of money involved.

This means that both parties, the payer, and the payee, use electronic mediums to exchange money.

Types of Digital Payments

Source: https://www.nielit.gov.in/content/digitalpayments

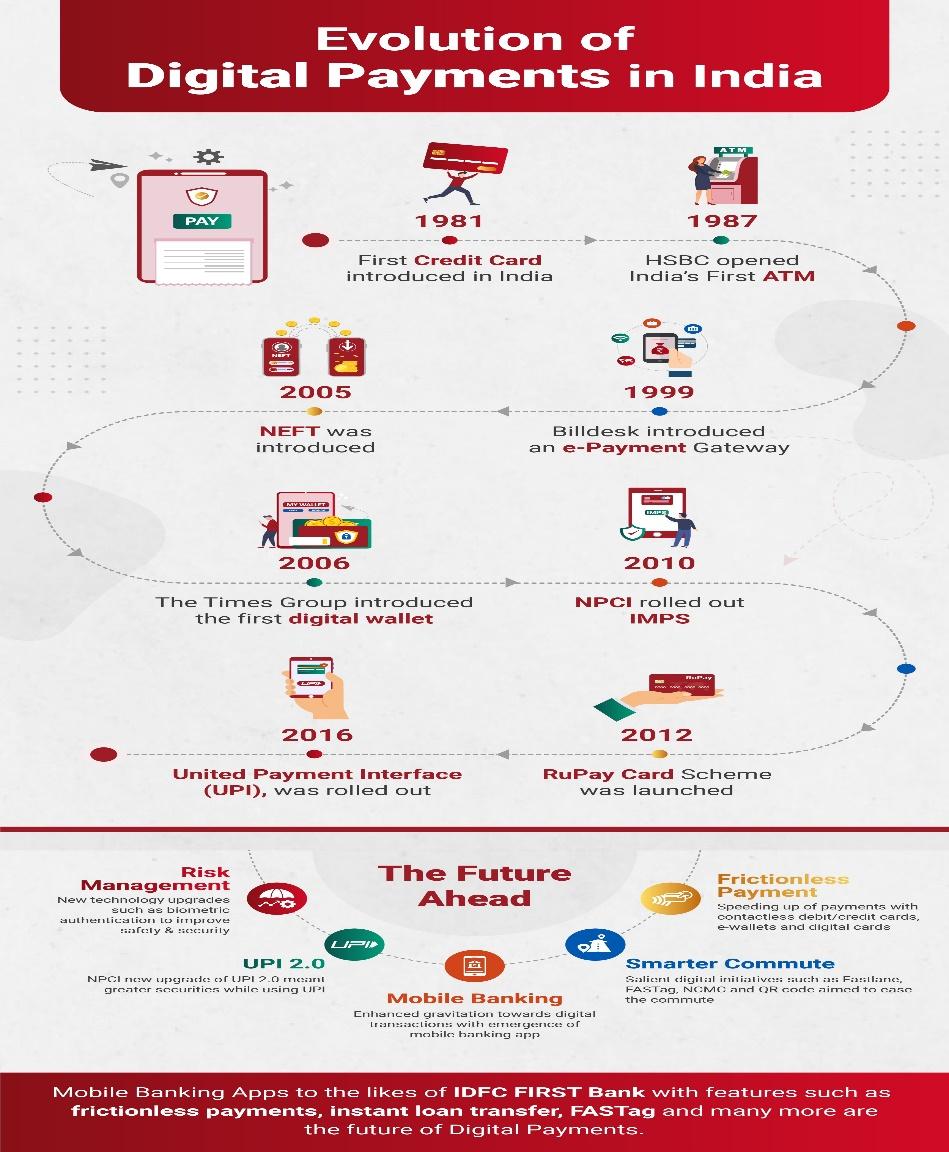

Evolution of digital payments in India

In India, though the payment system was mostly through cash and in bank transfers it lacked transparency and accountability unlike western countries where the payments are cashless and having a unique identification number to track their records.

On 1st July 2015, the Prime Minister Mr. Narendra Modi launched Digital India, where the vision of Digital India programme is to transform India into a digitally empowered society and knowledge economy.

UIDAI

On 12th July 2016, as the first step towards digital vision, Unique Identification Authority of India (UIDAI) was launched by the Government of India, under the Ministry of Electronics and Information Technology (MeitY).

The Aadhaar Act 2016 has been amended by the Aadhaar and Other Laws (Amendment) Act, 2019 (14 of 2019) w.e.f. 25.07.2019.

UIDAI was created to issue Unique Identification numbers (UID), named as “Aadhaar”, to all residents of India.

The UID had to be (a) robust enough to eliminate duplicate and fake identities, and (b) verifiable and authenticable in an easy, cost-effective way.

As on 31st October 2021, the Authority has issued 131.68 crore Aadhaar numbers to the residents of India.

Increase in usage of digital payment post Covid

In November 2016, the demonetization of 500- and 1000-rupees notes brought a huge shockwave across the country.

Though there were both plus and minus related to the step taken, the main aim was to remove black money and make the system more transparent and accountable.

After some initial jitters, the country has started to adopt the alternative solution – digital mode of payments.

While many people have been using digital payment methods even before demonetization, the count has significantly increased after that.

But still, it was not able to curtail the black money and conceptualize the unified identification system as expected.

Later in 2020, when the pandemic of coronavirus started it created a major transformation among the people from the street vendor till multi-level supermarkets to encourage the use of digital mode payments to avoid contradicting the virus.

From then till now the growth of usage of digital mode of payments have been phenomenal.

The linking of Aadhar and Pan card to the Bank account has made the system more accountable and transparent which was the main motto of “Digital India” from the very beginning.

Source: https://www.idfcfirstbank.com/finfirst-blogs/finance/How-are-digital-payments-evolving-in-India

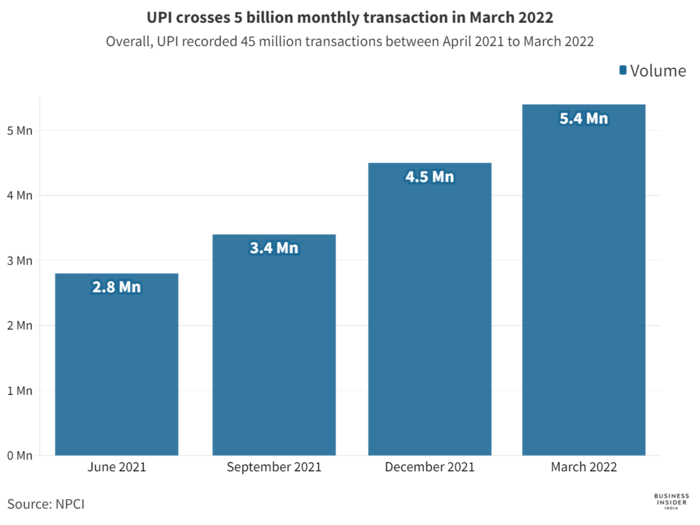

Growth of Digital payments

Source: https://www.openpr.com/news/2409036/india-payment-services-market-industry-market-revenue

UPI (Unified Payment Interface)

Unified Payments Interface (UPI) is an instant real-time payment system developed by National Payments Corporation of India facilitating inter-bank peer-to-peer and person-to-merchant transactions.

Aadhar Enabled Payment System (AEPS)

Aadhar Enabled Payment System, or AEPS, is a bank-led payments model that is based on the unique identification number and allows Aadhar card holders to make financial transactions through Aadhaar-based authentication.

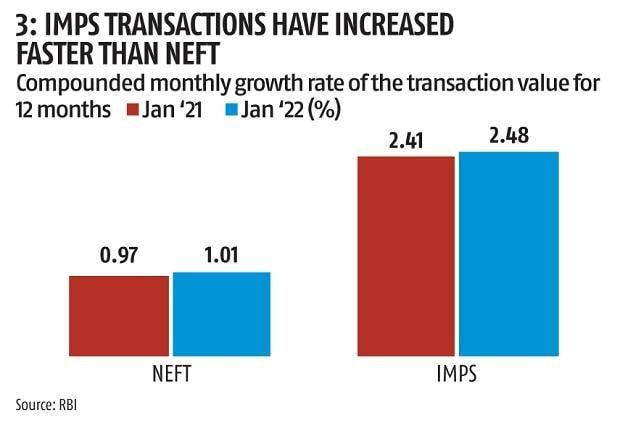

IMPS

Immediate Payment Services, or IMPS, is an instant interbank electronic fund transfer service through mobile phone.

One can access IMPS through multiple channels like mobile banking, SMS, net banking and even ATM.

While there is no cap on the minimum transfer amount, the maximum amount you can transfer per day through IMPS is ₹200,000.

FASTag

FASTag, founded in 2014, is an electronic toll collection system in India that is operated by the National highway Authority of India.

It employs Radio Frequency Identification technology to make toll payments directly from a prepaid or a savings account linked to the FASTag.

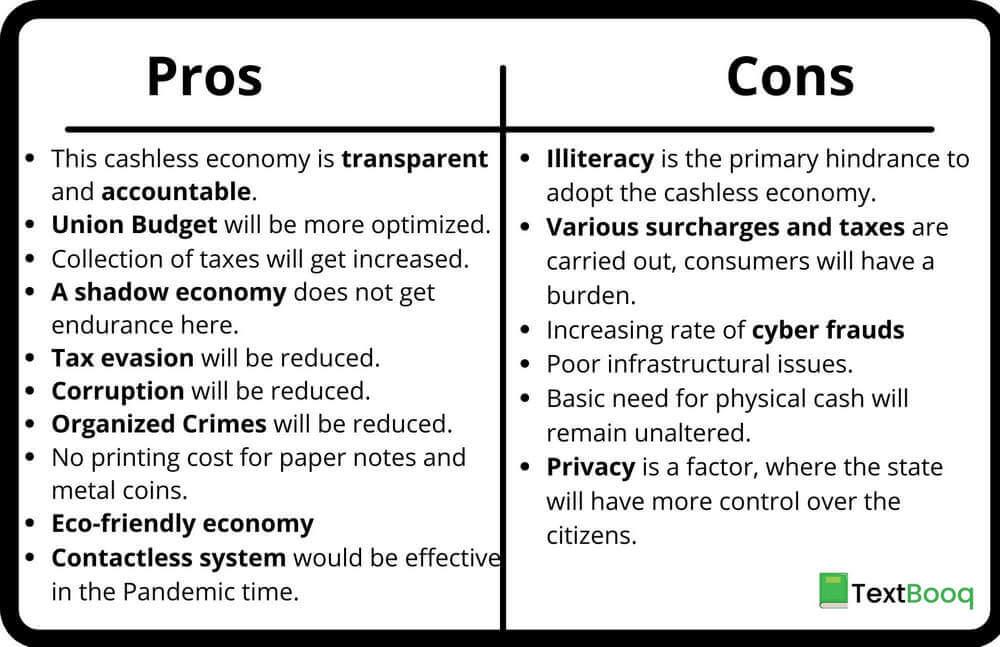

Pros and cons of digital payments

Source: https://www.textbooq.in/advantages-and-disadvantages-of-cashless-economy.html

Conclusion

We have seen a phenomenal growth in the usage of digital mode of payments over the past two years.

Slowly we are striving towards the motto of “Digital India”, but it can be completely achievable only with help of both the Governments, and the citizens of India.

Some still prefer cash over digital mode due to their reluctances in using the digital modes of payments but as they say, “All things are difficult before they are easy.”

So have awareness about it and its uses and be alert regarding the fraudulent activities and the ways to protect your money from cyber threat.

Hope you all enjoyed reading the blog, see you s